profit and loss + balance sheets

The purpose of final accounts is to give a 'snap shot' of a company's financial position at a given point in time.

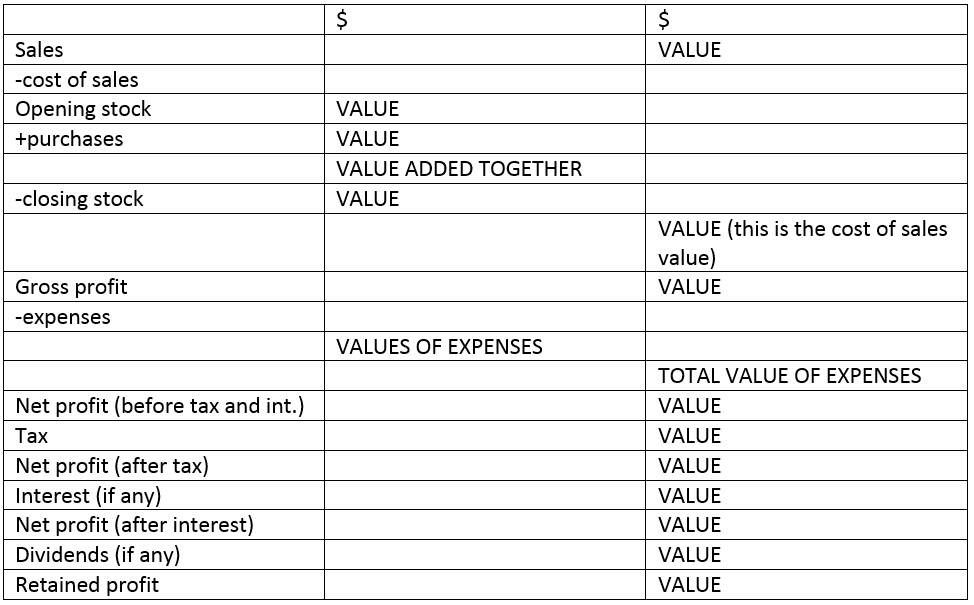

PROFIT AND LOSS ACCOUNT LAYOUT:

PROFIT AND LOSS ACCOUNT LAYOUT:

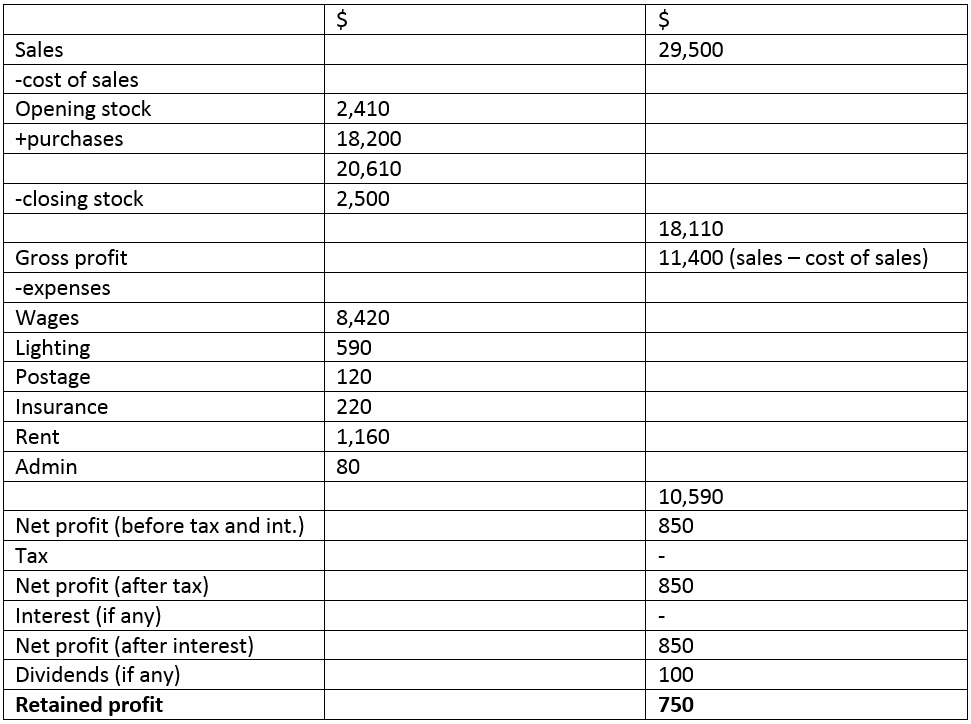

EXAMPLE:

Balance sheet requirements

Fixed assets

Items that the company owns and does not intend to sell - FAs help the business provide goods and services:

Current assets

Items that the company owns and intends to turn into money:

Current liabilities

Short-term debts that the firms owes:

Long-term liabilities

Long-term debts that the firm owes:

Shareholder funds

A firm's long-term finance owed by the company to its shareholders:

Fixed assets

Items that the company owns and does not intend to sell - FAs help the business provide goods and services:

- land

- premises

- machinery

- plant

- vechiles

Current assets

Items that the company owns and intends to turn into money:

- stock (raw materials/components, partly finished stock and finished goods)

- cash (cash at bank and cash at hand)

- debtos (people who owe YOU money)

Current liabilities

Short-term debts that the firms owes:

- overdrafts

- short-term loan

- creditors (people who we owe money TO)

Long-term liabilities

Long-term debts that the firm owes:

- mortgage

- long-term loan

- debentures (long-term fixed interest loans)

Shareholder funds

A firm's long-term finance owed by the company to its shareholders:

- reserves

- retained profit

- shareholders capital

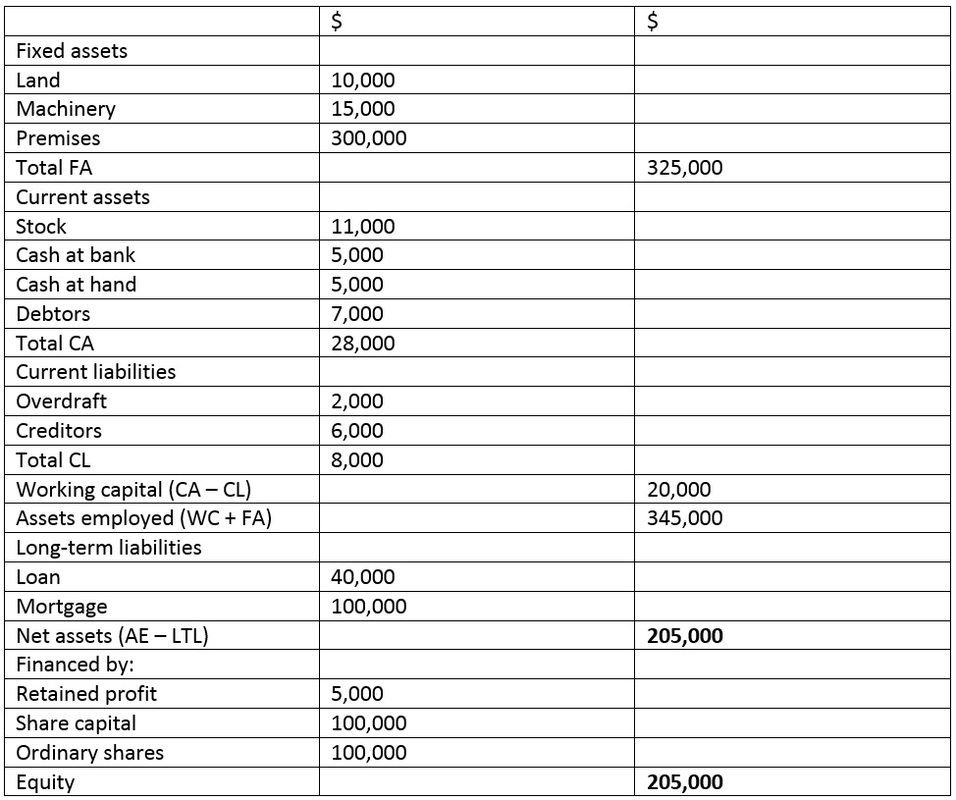

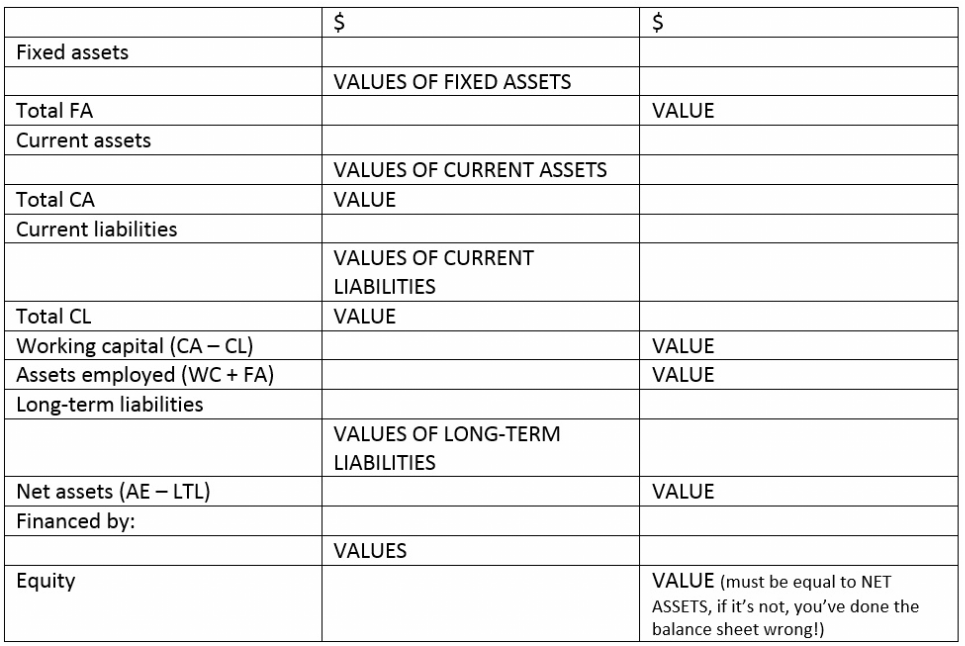

BALANCE SHEET LAYOUT:

EXAMPLE: